Could the U.S. steel market, characterized by elevated prices and diminished production levels recently, stand at the precipice of change? Futures data suggests a shift could be imminent, propelled by the intricate dynamics of imports, fluctuating raw material costs, and evolving market expectations.

Steel prices in the U.S. remain elevated, with current prices around $1,100/ton, nearly double that of other regions around the globe.

Despite higher prices, U.S. steel mills are cautiously maintaining subdued production levels, operating at a conservative capacity utilization rate of around 73.1% as of early January.

Low import volumes have contributed to tight market conditions. However, with lagged data showing restrained imports until October, a potential shift is anticipated as more recent import data might reflect an increase.

This shift could be influenced by the attractiveness of imports due to lower domestic pricing, likely impacting inventory dynamics and potentially slightly elevating import costs.

Market indicators, particularly the futures curve, suggest that higher prices could be temporary. Futures data indicates a gradual decline over the coming months as certain market factors begin to self-correct. This sentiment could align with the expectation of a potential seasonal weakening beyond Q1.

A recent Ryerson customer survey indicated that over the next six months, 64% said they planned to maintain their current level of spending on metal. Roughly 27% say they plan to increase their metal spending in the next six months, while only 11% planned to decrease their spend in this timeframe.

Stainless Steel Pricing Trends in 2024

Three commodities that shape the price of stainless steel are nickel, chrome, and molybdenum. Let’s look at market dynamics shaping each as we begin 2024.

The more things change, the more they tend to stay the same for the global nickel market. A five-year chart of LME nickel indicates that the current nickel prices are close to 52-week lows, around $7.30. This contrasts with the exceptionally high prices of $25 per pound during a short squeeze in 2022. The key driver for the current nickel market conditions is the increased availability of nickel, particularly class one nickel, with Indonesia ramping up production.

We have seen a significant growth in the nickel volume hitting exchanges, particularly the London Metal Exchange (LME). This is attributed to increased production in Indonesia and the LME's efforts to fast-track the inclusion of more grades of class-one nickel on the exchange.

According to Nick Webb, Ryerson’s director of risk management, and commodity hedging, the growing nickel inventory on exchanges may signal that the market no longer faces a shortage of class one unit.

“The excess nickel might not be immediately consumed in end markets, potentially indicating weak demand,” says Webb. “Instead, the nickel produced might be stockpiled in warehouses rather than utilized in stainless steel production.”

Despite these conditions, Webb remains cautious about the outlook for stainless steel for most of 2024. He says that if nickel prices continue to decline, it’s possible that Indonesia will reconsider its current production levels.

On the molybdenum front, South American production issues are causing tightness, leading to a $25/lb. peak. However, prices have since decreased to approximately $17.25 to $17.50 per pound. The trend suggests some softness and sideways movement in molybdenum prices.

For chrome, the South African chrome index, while not the official index for North American stainless surcharges, serves as a directional indicator. Some are forecasting a potential 4-5% softness in chrome prices on a quarterly basis, settling around $145 or $150/lb. This suggests a relatively stable but slightly declining trend.

(Source: Bloomberg)

Alumina Impacts Aluminum Pricing

The aluminum market has been experiencing a series of events that are reshaping the supply-demand balance and impacting pricing dynamics.

As of late, there has been a notable 7-8% increase in the price of LME ingot, a crucial component influencing the price of common alloy aluminum. A significant driver of this trend has been the price movement of alumina, a key material in aluminum production.

Much like iron ore is essential for steel manufacturing, alumina is integral to the production of aluminum. Derived from bauxite, the two primary raw materials in this process, alumina undergoes refinement before being utilized in aluminum production.

Environmental and regulatory concerns in China led to a curtailment of alumina production, contributing to the market's tightening. Additionally, a major explosion occurred at a bauxite facility in Guinea. These two incidents, though possibly short-term in their impact, have had tangible effects on the market.

While the percentage change in alumina prices may not seem substantial in the context of the volatile past five years, recent moves, such as a 25% increase in China and a 10% surge in Australia, are meaningful. These fluctuations are acting as a cost-push mechanism influencing LME aluminum prices.

Traders are taking note of these developments, as indicated by the Commitment of Traders report, a metric reflecting the sentiment of the financial community. Until early December, there was a bearish stance, with short positions dominating. However, that sentiment has shifted towards marginal bullish territory, influenced by factors related to the raw materials crucial for aluminum production.

Supply Chain Trends in 2024

Is the worry about future supply chain disruptions diminishing? Despite indications from a national index pointing towards a return to normalcy, the potential impact of geopolitical tensions might contradict such optimistic expectations.

The Federal Reserve's Supply Chain Pressure Index indicates a shift in supply chain conditions. The index, which typically ranges between negative one and one during normal times, peaked above four, signifying significant deviations from the norm.

As of the latest data point, the index stands at 0.11, suggesting that supply chains have returned to a more normal state. Just a few months ago, they were even somewhat loose, indicating an abundance of available goods. However, the speaker cautions against a potential resurgence of disruptions, highlighting the need to monitor the situation closely.

One concerning factor is the current geopolitical situation affecting international shipping. Tensions, possibly involving Iran and other Middle Eastern nations, have led to disruptions in the Red Sea and the Suez Canal. This conflict has forced vessels to divert south, circumventing the southern tip of South Africa and adding considerable time and expense to shipping routes.

This conflict impacts the flow of goods through crucial shipping channels, leading to increased costs, longer lead times, and potential shortages of shipping containers. While not reaching the scarcity levels observed in 2021 and 2022, the situation is evolving rapidly, and further escalation could exacerbate supply chain disruptions, causing inflation in shipping costs and delays in the delivery of goods and services.

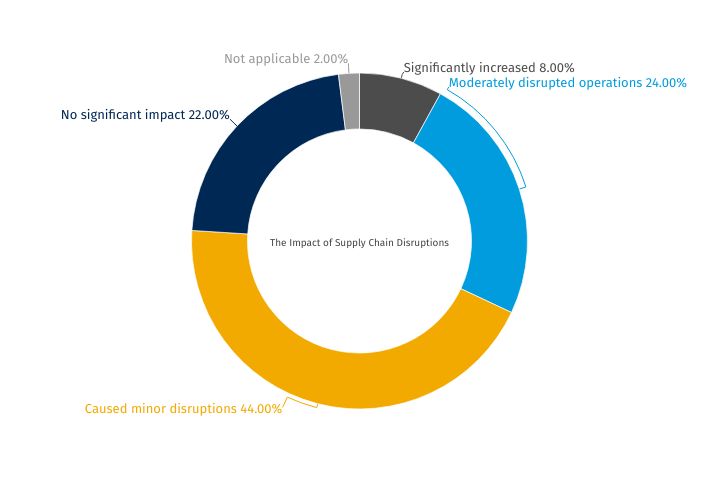

In a recent survey of Ryerson customers, nearly a quarter of respondents acknowledged facing moderate challenges, whereas only 9% highlighted encountering significant challenges. Approximately 23% indicated that supply chain disruptions had no notable impact on their business in 2023.

Ryerson: The Metal Supplier of Choice

Ryerson is a leading North American metal supplier that provides more than just metal. We respond to the ever-changing needs of manufacturing today.

With a vast inventory of steel, stainless, aluminum, alloy, and more, we are committed to providing our customers with the metal and services they need to succeed. We stock a range of shapes and sizes, or we can provide processing and fabrication for every product we sell.

Order online at Ryerson.com for comprehensive pricing and fast delivery, or contact us today to learn more about how we can meet your metal needs.